Sunday, 26 Jul, 2026

By: Rishav Khetan

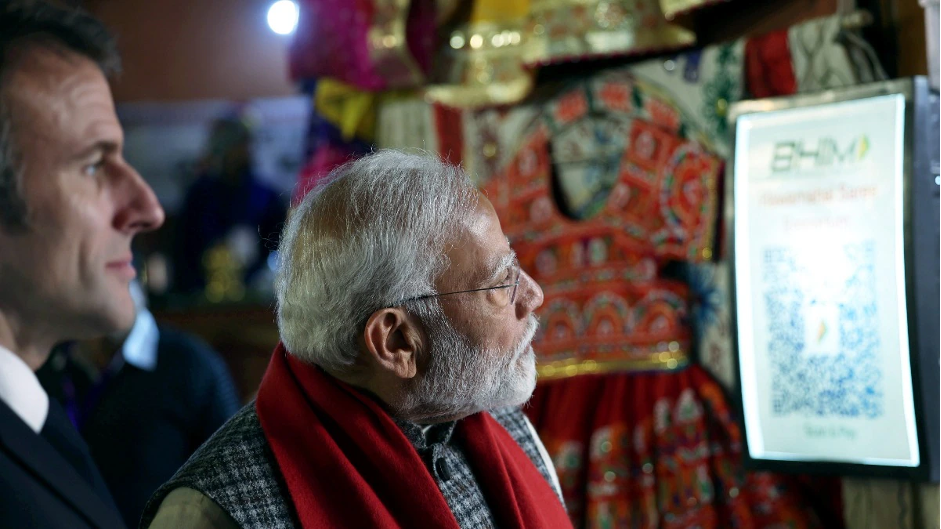

Source: Press Trust of India (PTI) | PM Modi demonstrates India's UPI system to President Macron in Jaipur, Rajasthan, by purchasing Kulhad tea and an Indian handicraft using UPI.

UPI has emerged as a preferred payment solution, witnessing over a billion transactions monthly, as per RBI, UPI’s share in India's digital payments surged close to 80% in 2023. Transactions through UPI in India surged to unprecedented levels in the Financial Year 2023-24, witnessing a remarkable 57% increase in volume and a substantial 44% rise in value compared to the preceding financial year.

The Unified Payment Interface (UPI) has emerged as a ground-breaking Indian innovation, garnering international attention and transforming the nation's digital landscape. Spearheaded by the incumbent Bharatiya Janata Party government led by Prime Minister Narendra Modi, UPI has revolutionized domestic transactions and positioned India in the global leadership in digital payments. With billions of transactions conducted monthly, the Indian government aims to elevate UPI into an indigenously built international payment system. However, this ambitious plan faces significant challenges ahead, with the global payment giants competing to capture domestic and global markets.

Launched in April 2016 by then-RBI Governor Dr Raghuram G Rajan, UPI has since become an integral part of the Indian Banking system. The impetus for digital payments gained momentum following demonetization and the Digital India initiatives. To facilitate seamless digital transactions, the National Payment Corporation of India (NPCI) introduced the Unified Payment Interface as a cost-effective solution for enabling digital payment services. The government's special emphasis on the Digital India scheme spurred major structural reforms in the banking sector, augmenting the usage of information and communication technology to digitalize the economy. In recent years, substantial improvements in digital infrastructure, coupled with enhanced internet connectivity and technological advancements, have further propelled the adoption of digital payment methods across India. According to the Reserve Bank of India (RBI), as of February 2024, approximately 560 banks were actively participating in the UPI ecosystem.

Digital India: Driving Economic Growth

The success of digital payment in India, including UPI, is a remarkable story in itself. The adoption of digital transaction methods among citizens has surged, driven by their perceived safety, reliability, and convenience. The volume of digital payment transactions has witnessed a staggering increase, surging from 2,071 crores in FY 2017-18 to 13,462 crores in FY 2022-23, indicating a remarkable compound annual growth rate (CAGR) of 45%. The digital transactions have already surpassed 16,800 crores during the current FY 2023-24 up to 31st March 2024. Concurrently, the year-on-year growth rate in the value of banknotes in circulation has shown a decline, dropping from 9.9% in FY 2021-22 to 7.8% in FY 2022-23.

UPI has emerged as a preferred payment solution, witnessing over a billion transactions monthly, as per RBI, UPI’s share in India's digital payments surged close to 80% in 2023. Recent data from NPCI unveiled transactions worth Rs 18 lakh crore conducted through UPI in February 2024, with a staggering 122 crore transactions. The growth of UPI can be gauged from the fact that it took four years for the monthly value of UPI transactions to exceed Rs 3 lakh crore since it was first launched in 2016, but in the next one year, it has more than doubled its transactional value to Rs 7 lakh crore. Transactions through UPI in India surged to unprecedented levels in the Financial Year 2023-24, witnessing a remarkable 57% increase in volume and a substantial 44% rise in value compared to the preceding financial year. A recent report by the Boston Consulting Group (BCG) indicates that India's digital payment sector is poised for substantial growth. The market is projected to expand from its current value of $3 trillion (Rs 226 lakh crore) to $10 trillion (Rs 750 lakh crore) by 2026. This sentiment is echoed by PricewaterhouseCoopers (PwC), which forecasts that daily UPI transactions could surge to 100 crore by the fiscal year 2026-27. Dilip Asbe, MD and CEO of NPCI and the mastermind behind UPI technology, envisions a future where a billion transactions per day are possible through UPI, a significant jump from 22 crore transactions per day right now.

UPI Goes Abroad: Ambitions and Challenges

In line with the government's vision of promoting indigenous technologies on a global scale, significant efforts have been directed towards internationalizing UPI. According to data from MyGovIndia, India led the global digital payments landscape, recording a staggering 8.95 crore transactions in 2022, followed by Brazil, which amounted to 2.92 crore transactions, while China trailed in third place with 1.76 crore transactions.

The potential for international acceptance of UPI offers transformative opportunities, not only enhancing convenience and access to funds for Indians but also delivering economic benefits to countries with significant Indian travelers and diaspora. Nations across the Middle East and Southeast Asia have expressed keen interest in collaborating with India to establish domestic card schemes and real-time payment systems. To facilitate this expansion, NPCI has launched its wholly-owned subsidiary, NPCI International Payments Ltd. (NIPL), with the aim of venturing into international markets and collaborating on payment systems with partner countries. Currently, UPI transactions are operational in seven countries, including Bhutan, Nepal, Sri Lanka, Mauritius, the UAE, Singapore, and France, marking a significant milestone as UPI makes its debut in Europe with its entry into France. TerraPay, a global payments infrastructure company, established a partnership with NIPL to enable Indian customers and merchants with an active UPI ID to make cross-border payments at TerraPay-enabled QR sites internationally.

Ignoring data for a moment, the widespread presence of UPI QR codes at local tea stalls or vegetable shops stands as the most prominent indicator of UPI's success. As UPI ventures into the global market, it faces substantial challenges, including fierce competition from established giants like Visa and Mastercard, which currently dominate the global payments landscape. These companies have extensive networks, partnerships, and brand recognition worldwide, presenting a formidable barrier to UPI's expansion. Additionally, emerging players like Brazil’s PIX further intensify the competition. Launched by the Central Bank of Brazil, PIX offers instant payment solutions similar to UPI. It has gained popularity not only in Brazil but also in other Latin American countries and Canada. Overcoming regulatory complexities across international borders, establishing trust among diverse stakeholders, and ensuring seamless interoperability pose formidable challenges. Moreover, integrating UPI with various payment systems and digital platforms worldwide demands sophisticated technological solutions. Despite several hurdles, UPI has established itself as an innovative payment solution interface and has positioned itself as a mascot for the government's “Local to Global” initiative.